Michael Pascoe: Jim Chalmers must reckon we’re a nation of chumps

Jim Chalmers has played the Australian public for fools, writes Michael Pascoe. Photo: TND/Getty

Last month’s Reserve Bank interest rate rise is looking increasingly lonely, leaving the board with a tough decision this Tuesday: do nothing, which would look like admitting the November increase was a mistake – or double down on that mistake.

Meanwhile, Jim Chalmers was playing us all for chumps on Thursday, carefully not quite answering a question about the inflationary impact of the looming Stage Three tax cuts.

The Treasurer hilariously created the impression that, somehow, inflationary pressures don’t matter if the Reserve Bank and Treasury know about them. Apparently inflation is only a problem if it unexpectedly jumps out of the bushes and says “Boo!”, catching us by surprise.

Well, it was hilarious if you thought about it for a moment.

Caught between a rock (breaking an election promise) and a hard place (making inflation worse), Mr Chalmers is going with the hard place and pretending it doesn’t matter, fudging rates being higher for longer because of the political pressure exerted by the rock.

On ABC Radio National, Patricia Karvelas specifically asked Mr Chalmers if he was worried the Stage Three tax cuts would be inflationary.

In a triumph of form over substance, the Treasurer effectively said he wasn’t worried about whether they would be inflationary because he already knew they would be inflationary. Or in his own words:

“The impact of these tax cuts, because they were legislated so long ago, they have been factored into the base line of the Reserve Bank’s inflation forecasts. Indeed, the Treasury inflation forecasts as well.

“So they are baked in because they were legislated some time ago when it comes to the Reserve Bank or the Treasury’s assessment of inflation.”

There was no attempt to deny the undeniable – of course, pouring an extra $21 billion of demand into the economy next financial year will add to inflationary pressures and therefore keep interest rates higher for longer – but, you know, it’s OK, because, well, we know.

It’s a minor point that Mr Chalmers was misleading in suggesting the RBA had factored in the tax cut impact in its forecasts way back in the day.

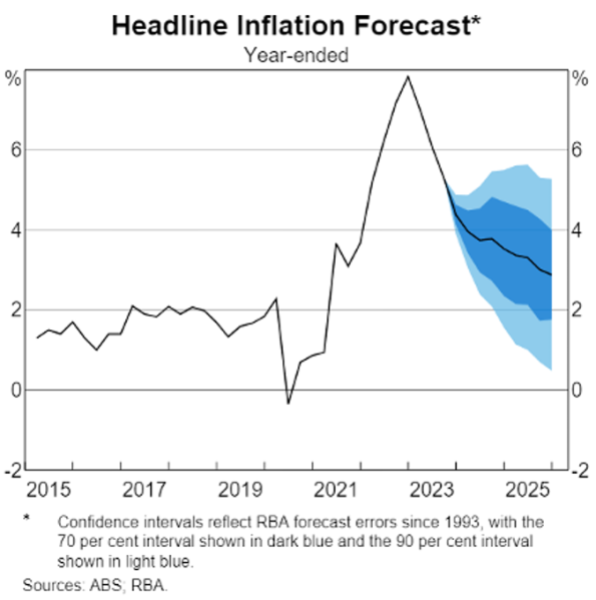

As we discovered in the bank’s November Statement on Monetary Policy, the RBA seems to have only just realised that the tax cuts are about to happen.

The RBA’s CPI forecast from November 10.

In July, ex-Senator Rex Patrick lodged a freedom of information request with the RBA seeking “any analysis/briefs/reports/submissions by the RBA since 1 July 2022 about predicted effects of Stage 3 Tax Cuts on inflation and/or interest rates”.

The RBA replied that it could not find any such documents. So much for that long-since baked-in assessment, not that it’s relevant.

The November CPI forecast graph shows the inflation bump and slower decline from the second half of next year when the cuts start.

In the same RN interview, Mr Chalmers was taking some comfort from various predictions, including by the OECD, that the RBA rate cycle might have reached its peak last month.

Those predictions come as evidence mounts of a slowing Australian economy, a lower-than-expected monthly CPI measure from the Australian Bureau of Statistics and in the context of inflation internationally cooling.

American expectations are that the Federal Reserve is done with rate rises. Eurozone inflation was lower than expected in November, consumer prices rising at an annual rate of 2.4 per cent.

Both the Fed and the ECB began their rate pause before the RBA’s November meeting, leaving Martin Place as the odd one out with another 25-point rate increase.

‘They go around in pairs’

If the board was feeling a little lonely then, particularly when it had been citing sticky services inflation overseas as a reason, the usual aviary terms of “dove” and “hawk” will be joined by “shag on a rock” this month.

I’ve previously quoted the line from veteran economist Chris Caton that “interest rate increases are like nuns. They go around in pairs”. With expectations turning against it, Governor Michele Bullock will be hard pressed to find a second sister this Tuesday.

Another economist explained the rationale for the quote as one move not making a material difference: “Either this one is unnecessary or there’s more to come”.

It looks like the November hike was indeed unnecessary. Told you so.

Since then, Ms Bullock has strongly defended her first rate move as governor as necessary due to the strength of demand showing up in rising prices for services.

“Hairdressers and dentists, dining out, sporting and other recreational activities – the prices of all these services are rising strongly,” she somewhat infamously said.

Chew on this

Her bagging for that sentence has been unfair – she was not blaming people going to the dentist for inflation or telling them not to go.

Mentioning dentists was tin-eared by the Governor, though. Her speech was delivered the day after ABS figures showing an increase in people putting off seeing health professionals.

The ABS reported seven per cent of people who needed to see a GP in the past financial year either delayed or did not see one due to cost – double the figure in 2021-22.

It was much worse for dentists.

Of people aged 15 years and over in the most disadvantaged 20 per cent of the population, more than a quarter either delayed or did not use a dental professional when they needed to.

The figure was 22 per cent for the second quintile and still 18 per cent for the third.

That was for the 2022-23 financial year. If dentists’ prices have been “rising strongly” since then, presumably the figures would be worse now. Something to chew on.

Want to see more stories from The New Daily in your Google search results?

- Click here to set The New Daily as a preferred source.

- Tick the box next to "The New Daily". That's it.

Retiring without super can be a worrying prospect

Labor promises a ‘fairer’ gas deal