Ask the Expert: Protecting your retirement savings from a volatile market

Markets have always had big swings, and will continue to do so in the future. Photo: Getty

Question 1

Current global conflicts, especially in the Middle East, and Donald Trump’s unpredictability are creating chaos in the market, affecting stocks and shares.

As our super is invested in international shares, do you have advice for protecting retirement savings from catastrophe, for someone who is already of retirement age. We have no time to ride out the situation.

Should I take part of my super and put it away somewhere to protect it from being eroded by volatile markets?

Market volatility, where the value of your investments goes up and down with big swings, has always been around to some extent. Of course, sometimes it’s a lot more obvious.

It can be unnerving when the swings are big in the negative. Even more so as you approach, or are already in, retirement.

There are a few things to consider.

First, as mentioned above, markets have always had big swings, and will continue to do so. You need to put things into context and look at the big picture.

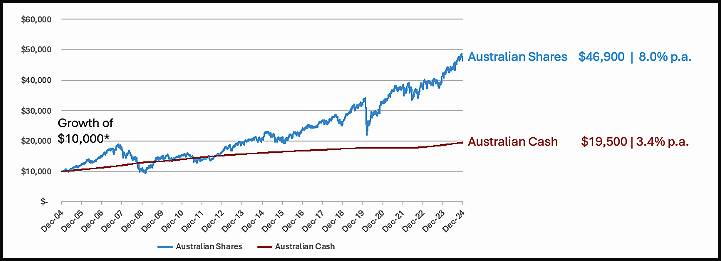

Our friends at UniSuper have provided the below charts.

First, the Australian share market versus cash over 20 years – as you can see, shares have outperformed cash by a long way.

You also need to consider the effects of inflation over that period of about 2.7 per cent a year. That means cash, after inflation, has returned about 0.7 per cent per year.

Source: Bloomberg, UniSuper. Australian Shares is the S&P/ASX 200 Total Return Index1 and Australian Cash is Bloomberg AusBond Bank Bill Index2. Daily return series applied. *Assumes income is reinvested and no fees, costs, taxes are incurred. Dollar figures are rounded to the nearest 100 for simplicity. Past performance is not an indicator of future performance.

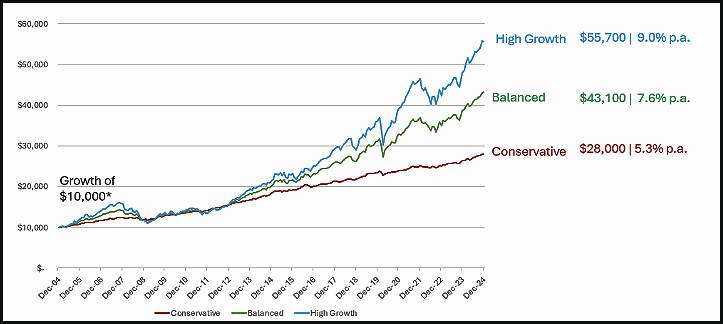

Second, in super, you generally choose an investment option(s), rather than investing directly in a market.

This graph shows how three of UniSuper’s pre-mixed options have performed. As you can see, the options with the most growth assets (Australian and international shares and property) have performed the strongest. This would be similar for all super funds.

Source: UniSuper. Conservative is the UniSuper Conservative Option – Accumulation; Balanced is the UniSuper Balanced Option – Accumulation; and High Growth is the UniSuper High Growth Option – Accumulation. Monthly return series applied. *Returns are after fund taxes and investment expenses but before account-based fees. Assumes income is reinvested. Dollar figures are rounded to the nearest 100 for simplicity. Past performance is not an indicator of future performance.

I take your point that you are already retired. However, I’m unsure of your age, investment option and how much you are drawing out of super each year.

When retiring, many people these days expect their super to last 20-30 years, so that’s still a long time frame!

To sum up, these are your options to consider:

- Choose an investment option that you feel comfortable with and stick with it, no matter what the markets do. Switching in and out of cash rarely makes sense. Neither does keeping most of your money in cash for a long period.

- Consider a lifetime annuity or pension. This is where you hand over a lump sum of money and in return get a guaranteed income for the rest of your life. These products are a lot more flexible than in previous years. However, you should look at putting only part of your funds into one of these and keeping the rest of your super flexible. These products have been underutilised and undervalued. The No.1 concern for retirees is running out of money. This really helps to solve that problem and reduces worries about investment markets.

- Speak with your super fund. All funds are required to have a published “retirement income strategy”. This is where they can provide tools, guidance, assistance and, in some cases, personal advice to members. You should contact it to discuss these options. If it can’t help, contact a financial adviser.

Question 2

Hi Craig, my wife and I are both retired at age 71.

We have a combined $760,000 in income stream accounts, $16,000 in accrual super accounts and $220,000 in bank accounts. Our personal assets would total about $50,ooo.

Would we be eligible for a part pension on these figures?

John

Hi John,

Given the information you have supplied, you are likely asset-tested rather than income-tested, as this provides the lower result.

You would both be eligible for a small age pension of about $30-$40 a fortnight each. Once eligible for the age pension, you also receive the Pensioner Concession Card.

As at September 2025, a couple who owns their own home can have other investment and assets valued up to $1,059,000 and still receive a part age pension.

The thresholds are indexed twice a year.

Craig Sankey is a licensed financial adviser and head of Technical Services and Advice Enablement at Industry Fund Services.

Disclaimer: The responses provided are general in nature, and while they are prompted by the questions asked, they have been prepared without taking into consideration all your objectives, financial situation or needs.

Before relying on any of the information, please ensure that you consider the appropriateness of the information for your objectives, financial situation or needs. To the extent that it is permitted by law, no responsibility for errors or omissions is accepted by IFS and its representatives.

Want to see more stories from The New Daily in your Google search results?

- Click here to set The New Daily as a preferred source.

- Tick the box next to "The New Daily". That's it.

Blend pension and super for comfortable retirement

Different view of pensions – and why they exist