Five super mistakes and how to avoid them

Your super savings can make a big difference in retirement — knowing the basics now can help you avoid costly mistakes later. Image: Dreamstime

When mandatory superannuation was first introduced in 1992, the required employer contribution (Super Guarantee) was a modest three percent of your salary. This amount is now 12 percent. Many people who are now approaching retirement have been ‘in the system’ for 33 years, so their savings are significant, with median balances of around $210,000 for singles and $418,000 for couples. So the stakes are high.

The age-old saying tells us that it’s not what you have, but what you do with it that counts. And that’s particularly true of how you save, nurture and manage your super. So what do you need to know to master the basics? There are five key things you can do right now to keep on top of your super savings. These actions will help you reduce expensive mistakes by avoiding:

- Disengagement, or not caring or not knowing how super actually works

- Failing to respond to your annual statement and so not boosting your super

- Not knowing how your total balance can convert now and in the future into retirement income (use calculator)

- Failing to take advantage of tax-savvy contributions rules, and

- Believing (mistakenly) that you will need way more than you actually will

It’s true that super can seem overwhelmingly complex at times, particularly the rules which influence Age Pension entitlements. But the challenge of better understanding super options has become much easier with the development of digital finance tools which do the sums on your behalf. Here is a short explanation of the five most important ways to take control of your super savings, regardless of your age or stage.

1. Avoid disengagement

Not to be confused with laziness, but that’s not what generally drives disengagement. More usually, disengagement is usually fostered by an inability to understand the basic mechanics of turning super savings into super income.

Many people incorrectly assume that – since super savings are mandatory – there’s nothing that they can do to enhance their financial outcome. This is incorrect. There are two main phases of super. The saving or accumulation phase and – once you can legally access your super (usually age 60 if retired, transitioning to retirement or otherwise meeting a condition of release, or unconditionally at 65), the spending or decumulation phase.

But there is also a ‘bridging’ period when you can start accessing super while still working and therefore, still contributing. By understanding the rules and working with your fund (and its advisors) you can ensure that you are saving as hard as you can and timing when you start to withdraw your savings to maximum advantage.

Read more about the ‘Transition to Retirement’ strategy here.

Your super statement is more than a balance update — it can help you plan your retirement income and investment strategy. Image: Dreamstime

2. Review and respond to your annual statement

Research house, SuperRatings, reports that only 55 percent of super fund members open their statements, which means that 45 percent will ignore them. Yet your annual statement is an invaluable summary of where you are at with your savings. This information allows you to project your likely retirement income. If this income is not as much as you had hoped, you can re-check that same statement to see how your assets are currently invested by your fund. This investment setting can then be considered alongside your attitude to risk and the number of years left before you will need to access these funds.

Many people who are years away from retirement are conservatively invested, which means their ultimate balance is probably going to be lower than it could have been. It’s also a prompt to review your contributions. If these are only the mandatory amount (12 percent), it’s time to explore whether you could take advantage of one of the strategies in Point 4 below.

Your super fund provides support to help you review and project. Here’s how.

3. Project how much income you will have in retirement

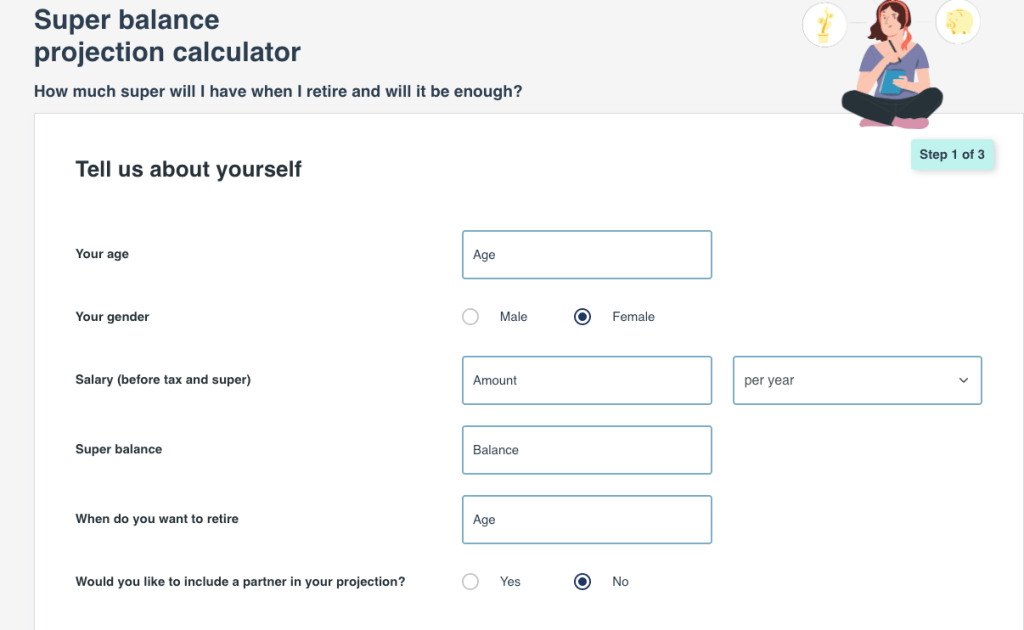

There’s really no excuse for not knowing your likely retirement income, given the excellent calculators available free of charge to all pre-retirees. One of the simplest to use is provided by Industry SuperFunds. You can find it here.

Use the retirement balance calculator to estimate your future super savings and better understand your retirement income outlook. Image: Industry SuperFunds

It allows you to input information on your (and a partner’s) current super balance, your age/s, your preferred retirement age, other financial assets. You can then let the calculator take over, predicting any Age Pension entitlements and how your super will help provide further income to create a reasonable retirement ‘wage’.

Income in retirement is usually a combination of Age Pension and super. This explanation helps cut through any confusion.

4. Take advantage of tax-savvy contributions rules?

We’ve spoken a lot about the legislated 12 percent Super Guarantee that is automatically paid into your fund by your employer. You are also able to ‘salary sacrifice” by paying pre-tax dollars into your fund up to the current cap of $30,000, but there are many other ways you can add to your super, including after-tax contributions.

Those who earn below $62,488 may be entitled to a government co-contribution, with the maximum amount of $500 payable to those earning $47,488 or less (provided they make a $1000 personal contribution). You do not need to apply for this amount – it’s assessed when you file your annual tax return and automatically credited to your super fund, if applicable.

There are also ways for couples to collaborate to maximise tax benefits when contributing to super.

More detail on tax and super can be found here.

Short videos and practical tools can help build your confidence and understanding of retirement income basics. Image: Industry SuperFunds

5. Don’t assume you’ll need much more than you have

It’s easy to feel despondent when you read media reports of the $700,000 or more you need for a so-called ‘comfortable’ retirement. That’s simply inaccurate – most singles have around the $210,000 and couples the $417,000 as confirmed by the Australian Tax Office in their annual summary of median retirement super savings. Yes, it could be challenging to live on this amount alone. But that’s not how the Australian retirement income system works.

About seven in 10 retirees start their post-work lives with an Age Pension entitlement topped up by income from their super savings. You can work out if you, too, will live on such a combination of funds by using the previously mentioned retirement balance projection. The beauty of the calculator is that it converts your savings into likely Centrelink entitlements plus a regular withdrawal through an Account-Based Pension or similar pension account when you begin the ‘spending’ phase.

The beauty of these five action points is that you can use them straight away. They are also supported by the calculators and basics glossary in the links provided. And should you need further detail or support then these short videos will also bolster your mastery of the basics of retirement income.

Get your head around your retirement at retiringbasics.com

Disclosure statement

This content is produced by The New Daily in partnership with Industry Super Australia.

This information provided in this article is of a general nature only and does not constitute financial or other advice. It is important to consider personal objectives, financial situations or particular needs when making financial decisions.

Want to see more stories from The New Daily in your Google search results?

- Click here to set The New Daily as a preferred source.

- Tick the box next to "The New Daily". That's it.

Blend pension and super for comfortable retirement

Different view of pensions – and why they exist

Super growth after retiring is great, but not a must