Housing affordability sinks to equal record low as first-home buyers priced out

New data shows housing affordability has sunk to a record low. Photo: TND

Australians are facing the worst levels of housing affordability on record as soaring property values increasingly price average income earners out of the market, according to new data.

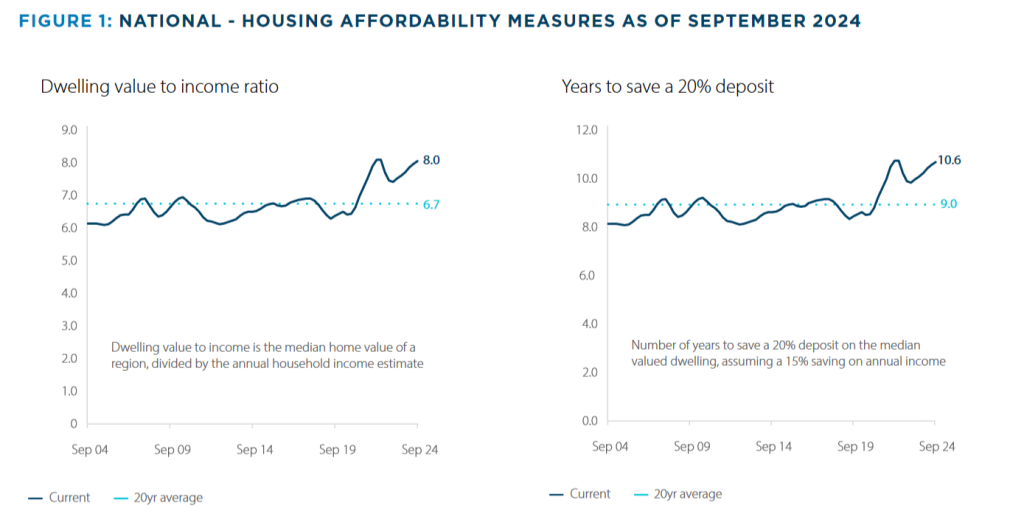

Analysis published on Wednesday by ANZ Bank and CoreLogic revealed that it takes 10.6 years of earning the median income and saving 15 per cent of it a year to afford a median deposit.

Gross household income has risen 2.8 per cent over the past year, researchers found, but wages are “well below” the 8.5 per cent increase in median dwelling values in the same period.

It means only 10 per cent of the housing market is still affordable for households earning median incomes, down from 40 per cent in 2022.

No houses are affordable for lower-income families.

Housing affordability is now equal-worst on record with the spike in property prices back in 2022.

The ANZ/CoreLogic research also found things have become more difficult for Australians on either side of the first-home buyer experience too, with rents squeezing savers and high interest rates hurting those who have just bought.

“A record-high 33 per cent of income is needed for the median income household to service the median rent [which is now $642 per week],” researchers said.

“Assuming current average mortgage rates for owner-occupiers, a 20 per cent deposit and a 25-year loan term, more than half of the median household income is required to service a new home loan.”

Source: CoreLogic/ANZ

The figures are grim reading for millions of Australians increasingly worried about not being able to purchase property and the longer-term implications that has for financial security in retirement.

TND reported earlier this week that intergenerational inequality is rapidly worsening as young Australians bear the brunt of the cost-of-living crisis and the soaring price of buying a home.

Experts say federal reforms that include adjusting tax settings like capital gains discounts and negative gearing are needed to help address the problem, in addition to more social housing.

ANZ/CoreLogic researchers said that some Australians are navigating the housing crisis by buying cheaper homes and turning to the so-called “bank of mum and dad”.

But that is not available to everyone, which they said has wider distributional consequences.

“Not all first-home buyers have access to the bank of mum and dad, or some other means of wealth that can help them overcome the deposit hurdle,” researchers explained.

“As a result, access to home ownership may continue to become more concentrated in high-income, high-wealth households, a pattern that has been evident in the past.”

Housing affordability may improve slightly next year, with demand for property softening in recent months amid decade-high interest rates and wider cost-of-living pressures.

Some markets such as Melbourne, have experienced falling values, which may deliver some relief.

But the ANZ/CoreLogic researchers also warned that cyclical property market downturns don’t usually lead to “long-term improvements in housing affordability”.

“The declines eventually attract new buyers to the market. In the absence of a material increase to housing supply, this pushes values higher,” they said.

“Over the longer term, housing market ‘recoveries’ are likely for markets such as Melbourne.”

Want to see more stories from The New Daily in your Google search results?

- Click here to set The New Daily as a preferred source.

- Tick the box next to "The New Daily". That's it.

Reasons to be hopeful amid economic gloom

Jobless fall leaves door open to more rate hikes

The billionaire who failed Whyalla steelworks

Carveouts for business after budget backlash