Mortgage offsets on rise as households cope with higher interest rates

Banks say easing mortgage stress tests would boost affordability, but the idea has been labeled 'lazy policy' Photo: AAP

More Australians are opting for home loans with mortgage offset accounts as the cost of living squeezes budgets, but a financial adviser warns to keep a close eye on the interest rate.

National Australia Bank said this week that more than two-thirds of households are opting for offset accounts on their mortgages, with balances soaring by 55 per cent to $45 billion.

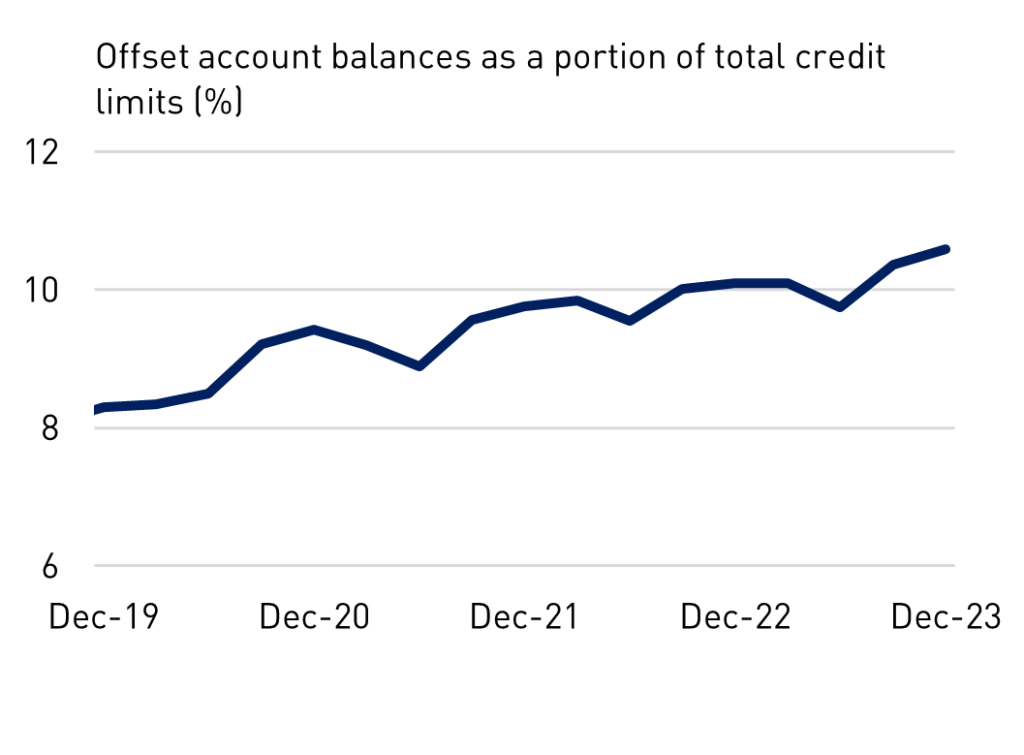

It comes after the latest official data from the prudential regulator showed that balances in offset accounts rose to 11 per cent of total credit limits over the March quarter, the highest since 2019.

Financial adviser and On Your Own Two Feet founder Helen Baker, said households have been using offsets to build up financial buffers in their home loans as interest rates have risen.

When rates are higher the value of each dollar in an offset account rises because it reduces the interest charged on a loan, making it more attractive for many than a traditional savings account.

“There’s a lot of uncertainty,” Baker said. “People are banking quite a bit of cash to protect themselves and also to try and get the interest down on their home loans.”

But beware, because offset accounts are a feature and often come with a higher base interest rate on your home loan than a mortgage without one, which makes your repayments bigger.

“You’ve got to do your numbers and look at your particular situation,” Baker explained.

Households build financial buffers

Mortgage buffers are a key reason millions of households have been able to cope with rapidly rising interest rates since Covid-19, with the Reserve Bank noting that home owners have been eager savers even amid the cost-of-living crisis.

Offset accounts are a natural way to do that for home owners with access to them, helping to cushion the blow of repayment increases and smooth out the effect on budgets over time.

Source: APRA.

“Offsets have been the secret weapon through a higher cost of living and interest rate rises and they’ve helped mortgage holders get ahead and stay ahead,” NAB’s home ownership executive Andy Kerr said.

But most recently there is evidence that savings are starting to run out for some households, with APRA’s latest data noting a small but material increase in loan stress in recent months.

Loans 30 to 89 days past due rose to 0.6 per cent of total loans over the March quarter, which was the fifth consecutive period that arrears rates increased, though it is still below historical levels.

Maximising offsets

Baker said that households that do have offset accounts should try to maximise them, because ultimately you’re paying extra to have one through a higher base interest rate on your home loan.

There are a few ways to do that.

The first tip is to have income deposited straight into the account.

You’ll also want to be as disciplined as possible and avoid – as far as you can – taking money out of the offset account, because the more savings you park in it the bigger the advantage for you.

It’s important to note, however, that offset accounts aren’t necessarily worthwhile for everyone.

You need to factor in the higher interest rate and ensure the savings you’re getting exceed the difference between that and any lower rate loan you could obtain without an offset account.

Baker explained that households need to “do the math” and seek financial advice about whether their savings could earn them a higher return if parked outside an offset account.

That potentially includes superannuation, which could be more attractive depending on the stage of your life.

Though for many households offsets are likely to offer a good return because it’s reducing your interest expense without incurring additional taxes.

“It’s going to be very difficult to get a return elsewhere, particularly with taxes involved,” Baker said.

Want to see more stories from The New Daily in your Google search results?

- Click here to set The New Daily as a preferred source.

- Tick the box next to "The New Daily". That's it.

The billionaire who failed Whyalla steelworks

Carveouts for business after budget backlash

Reserve hits brakes on rates, but remains wary

Musk becomes first trillionaire with SpaceX stock market launch

Musk’s SpaceX prices record $US75 billion IPO