How to avoid losing money in a bad investment

Source: Asteron Life

Every year, thousands of people get caught up in scams or are disappointed by their investments. The get-rich-quick variety are often delivered via cold calls, email or even investment seminars, while the more mainstream variety, such as hedge fund Trio Capital, were pushed by commission-driven financial planners.

The risks are only climbing as Australia’s superannuation pool climbs past the $1.7 trillion mark – the Trio Capital fraud, which was uncovered in late-2009, eventually cost more than 6000 super and other investors about $176 million.

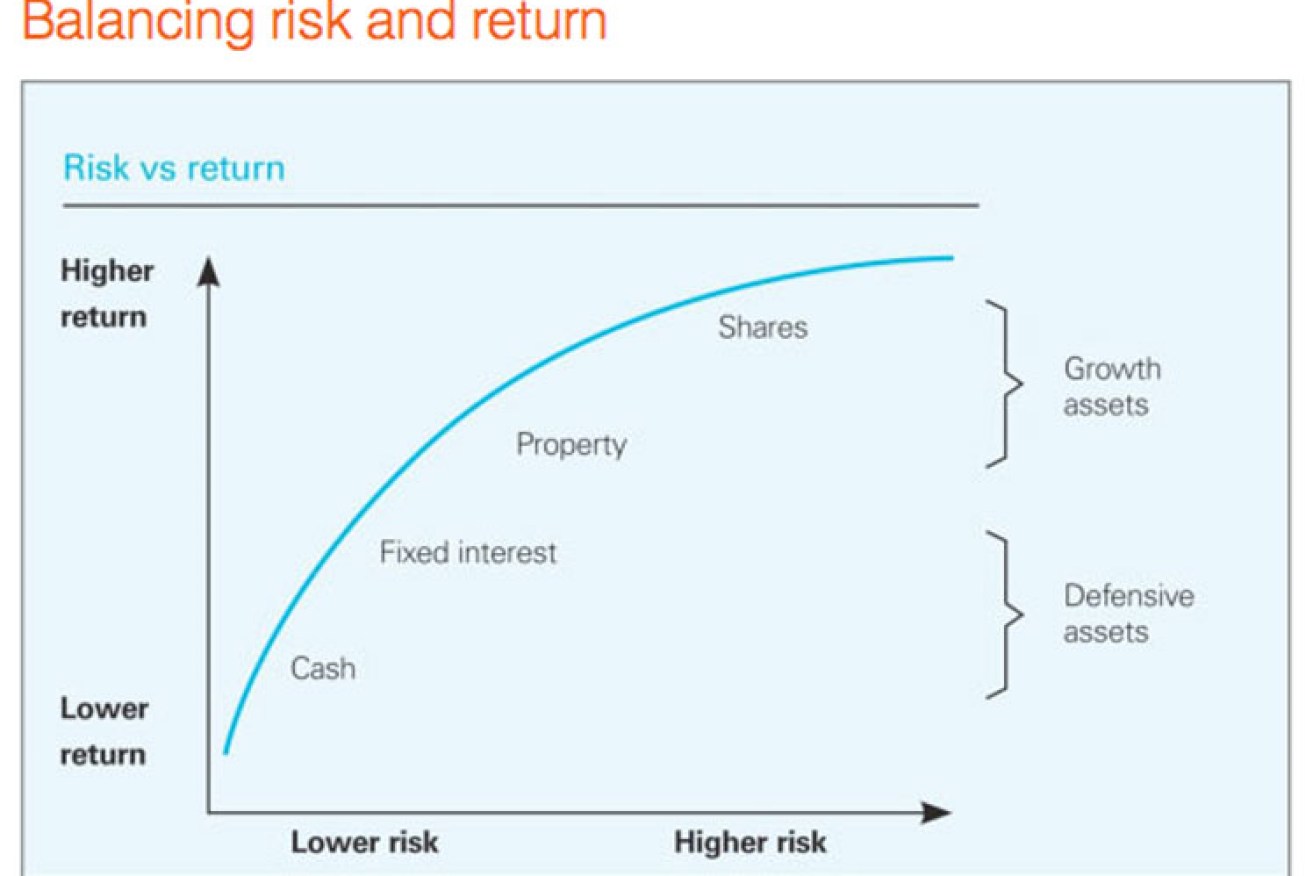

There are some basic checks investors should do to avoid such catastrophes – for example, every investment company should have an Australian Financial Services license. However, it’s still no guarantee that the touted investment returns on offer are realistic (Trio, as well as other recent investment disasters such as Storm Financial, were all licensed by the corporate regulator). But there is also a common-sense check that savvy, long-term investors rely on: There is a fundamental relationship between risk and return. The promise of higher returns comes with a commensurately greater chance of volatility and losses. A basic knowledge of the way each asset class behaves is crucial before making any investment decision.

Superannuation

The risk-return spectrum climbs across the major asset classes: From low-returning but safe cash through to higher-returning but more volatile shares and property.

Many super funds make the process of assessing risk and return easier by creating pre-mixed investment options that contain a blend of assets to better reflect their expected returns, such as conservative, balanced, growth and high-growth.

Super funds also now use a “standard risk measure” in their disclosure documents, which indicates the number of years that an investment option is expected to deliver a negative return over any 20-year period. It is not a guarantee but it is a good estimate.

For example, REST Industry Super’s core strategy (which is its balanced option) will deliver negative returns every 3-4 years over a 20-year period. Its cash investment option will produce less than 0.5 negative annual returns every 20 years, but its shares investment option is likely to produce six or more negative years over that same period.

The majority of investors will find their super invested in the balanced option, which contains about 60-70 per cent growth assets such as shares and property. It is a level that is high by global standards but should result in better long-term returns – an issue of real importance given the average life span continues to increase and most Australians will need to plan for decades of retirement.

However, a greater allocation to shares and property also results in greater volatility as many investors witnessed during the global financial crisis. It is the reason why the median balanced fund posted a 19.7 per cent loss in 2008 before gaining 12.9 per cent the following year, according to SuperRatings figures.

However, even with that volatility, long-term returns remain robust. Last year’s strong share market performance underpinned a 16.3 per cent rise for the median balanced super fund, while returns have now averaged 7.1 per cent a year over the past decade.

A better understanding of each underlying asset class can help investors make up their own mind.

Source: ASX, Russell Investments

Cash

The official cash rate, set by the Reserve Bank of Australia, is currently at an historic low of 2.5 per cent. It directly affects the price and interest rate of government bonds, where you effectively lend money to the government in return for a security which pays regular interest.

“Volatility does tend to be quite low – close to zero – and the odds of losing capital tend to be close to zero as well,” AMP chief economist Shane Oliver says.

“I’m assuming you’ve actually invested in cash as opposed to something masquerading as cash – years ago people were putting their money into hedge funds like Basis Capital prior to the GFC, which some seemed to think was a cash equivalent, but it was high risk.”

The official RBA cash rate is also the rate of interest the central bank charges commercial banks for overnight loans – it is a key component which affects the interest rates they set on deposits, mortgages and other products.

Some banks are still offering high-interest online savings accounts paying interest of about 4 per cent – albeit with plenty of strings attached, such as limiting the time before reverting to a lower interest rate.

Cash investments in super funds often return less than high-interest online savings accounts – currently about 2-3 per cent. However, they are not ripping you off – it’s just another example of risk and return.

Banks use deposits to fund their mortgages – a riskier investment practice than super funds, which often invest their cash balances directly in government bonds and similar assets. Super funds’ cash investments are also not included in the government’s bank deposit guarantee, which applies to deposits under $250,000.

Fixed Interest

Australian government bonds and bank deposits are at the safest end of the risk spectrum. Moving slightly up, there are a vast array of fixed interest securities: Semi-government bonds, corporate bonds and listed hybrids among them. Capital values can be affected by movements in official interest rates (their value goes down when interest rates go up) although holding fixed term bonds until maturity can negate that.

Companies issuing corporate bonds must pay higher rates of interest than the government because there is a greater risk they will hit financial trouble. A good rule to follow is the higher interest rate on offer, the higher the risk.

For example, listed bank hybrids, which can be traded on the Australian Securities Exchange, are popular among mum and dad investors because they pay higher rates of annual interest (currently 5-6 per cent). But, as always, such higher returns are generated with a greater risk of losses.

For example, bank hybrids include a clause that allows the Australian Prudential Regulation Authority to force the securities to be converted to shares if it believes the bank could become insolvent.

While it is a remote risk given the current financial strength of Australia’s big banks, it is one reason why most super funds do not invest in those particular hybrid securities and instead prefer to invest in other types of bank (and corporate) debt.

Property

Property is one of the most popular investments – the family home is often the biggest asset alongside super.

Residential investment property posted an average yearly return of 9.5 per cent a year over the 20 years ended December 2012, while listed property was only slightly lower at 7.1 per cent, according to the ASX.

Super funds generally invest in either listed property, which has some characteristics in common with shares, or direct commercial property, which is a long-term investment usually unavailable to mum and dad investors.

Property is valued far less often than other listed assets (aside from listed property), which can mask the volatility of capital returns.

“We have been reminded in the past few years that property prices can go down as well as up,” AMP’s Oliver says.

“Through the GFC and then from 2010 until 2012 property prices fell, even though the falls tend to be relatively stable and smooth over time you can see falls of up to 10 per cent.”

There are long periods when selling an investment property for a profit just isn’t possible and transaction costs can substantially higher than shares.

Shares

Shares are among the highest-returning asset classes, returning an average of 9.8 per cent a year over the 20 years ended December 2012, according to the ASX. Last year was even stronger, with the local market delivering a 15.1 per cent gain.

However, the risks of negative returns are high and it is one reason why investors should have a long-term outlook of seven years or more. Super funds are well suited to investors given they have such a long-term outlook and are well-placed to ride out the ups-and-downs of the market.

While investing in shares can be a bumpier ride than unlisted property, because it is valued more often, Oliver also says corporate earnings (which drive share prices) are more sensitive than property rental incomes, which tend to withstand downturns in the economy better.

Source: Asteron Life